Notary and Translation Sample

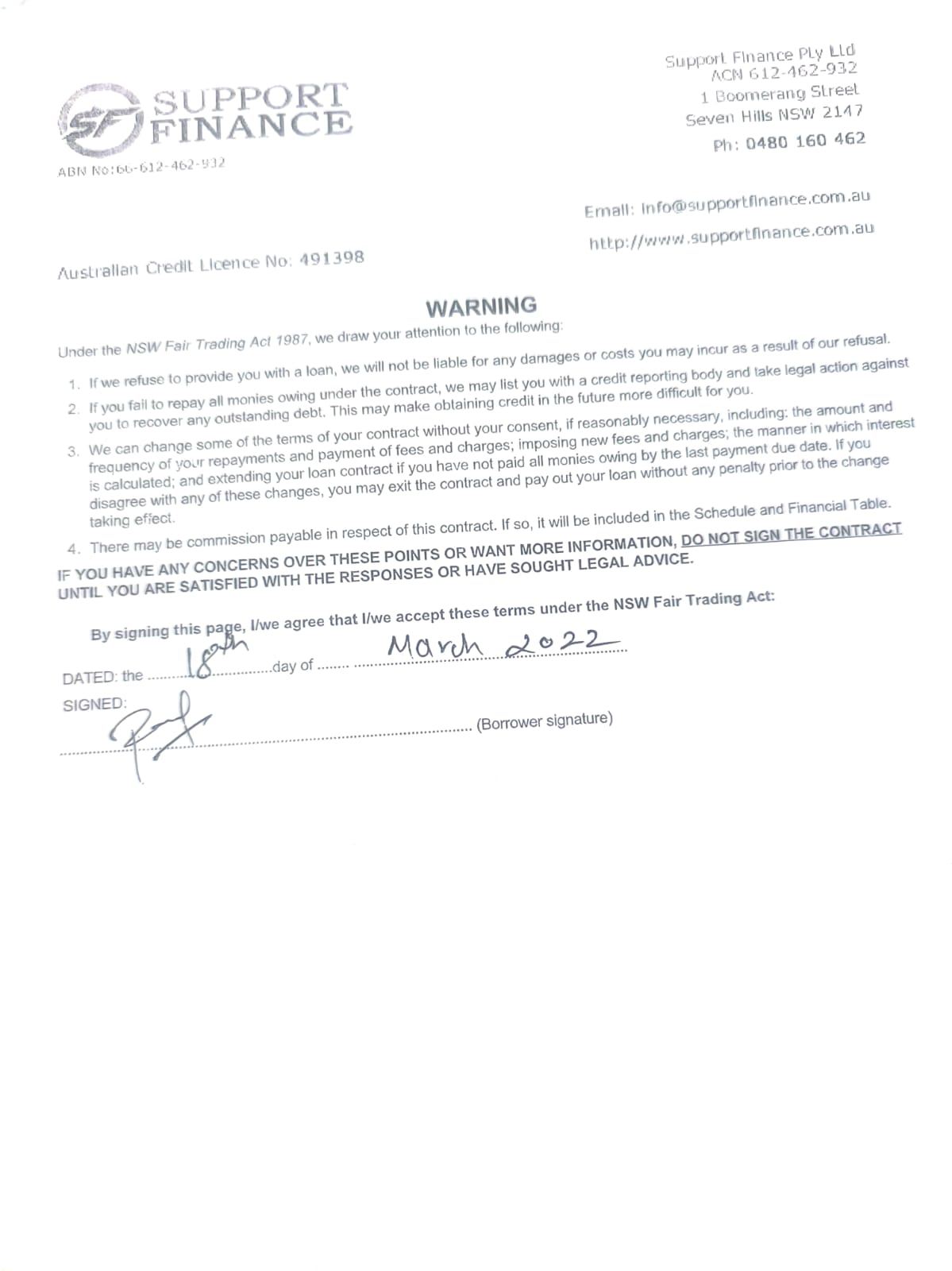

GENERAL RULES FOR YOUR LOAN

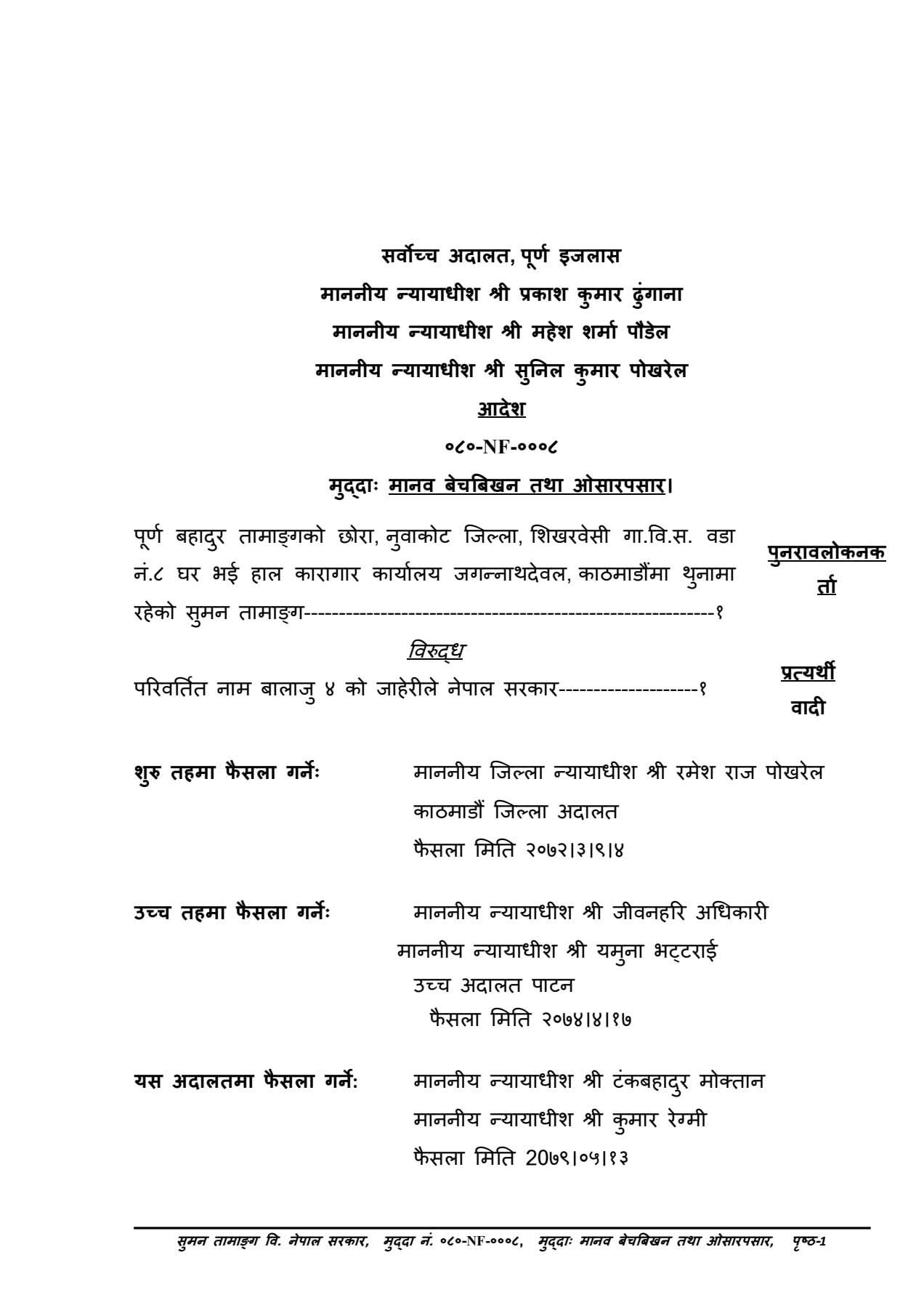

Notary Translation Sample (English to Nepali)

1. Requirements Before We Give You the Loan

We will only give you the loan if all the following conditions are met:

1.1. Before we give you the money, you must: a) Prove your identity clearly, using documents that help us follow all government rules. b) Satisfy us that the loan is right for your needs (not "unsuitable"). c) Show us that you can repay the loan without serious financial difficulty ("undue hardship"). This can be with information you or someone else gives us. d) Give us permission to get a satisfactory credit report from a credit reporting agency, if we decide we need one. e) Provide all other documents, materials, or information we ask for, and we must be happy with them. f) Convince us that you have truthfully told us about all other loans you currently have with other lenders. g) Confirm that all the statements and promises you made when you applied are true, correct, and not misleading. h) Sign the loan contract to officially accept our offer. i) We must also sign the contract. (We won't sign it until you do).

1.2. Debt Advice/Relief Check: You confirm that in the last 30 days, neither you nor anyone for you has talked to or applied to an accountant, financial advisor, counselor, planner, or any business offering debt relief, forgiveness, bankruptcy, or a debt agreement. If you have, you must tell us immediately before we finalize the loan.

1.3. Reasons We Might Cancel Before Signing: We will refuse to give you the loan if, at any time before we sign the contract: a) Something happens that we reasonably believe will negatively affect your financial situation or status. b) We find out that you hid information from us, or if we learn of any other fact that we think is important to the loan approval. If we cancel for these reasons, we are not responsible for any losses or costs you suffer.

1.4. Increased Government Fees: If any government fees or charges listed in the Schedule increase before the loan is finalized, we don't have to give you the loan until you agree to change the contract to cover the increased cost.

2. LOAN DETAILS

2.1. We agree to give you the loan for the reason you stated in your application.

3. REDRAW FACILITY

3.1. You cannot take out money again (redraw) or get more advances under this loan contract.

4. ACCOUNTS AND ADVANCES

4.1. We can put the loan money into your account, along with anything else your loan contract says we can charge to it.

5. INTEREST CALCULATION

5.1. Interest Rate: The yearly interest rate is 35.75%. This rate is divided by 365 to get a daily rate. * We calculate interest daily (to 9 decimal places) based on your outstanding balance. * Daily interest is added up (but not compounded) and the total, rounded to 2 decimal places, is charged to your account on the last day of each month. * We also charge interest on the day you pay off the whole loan.

5.2. When we add interest charges to your account, they become part of the balance on which future interest is calculated.

5.3. If we get a court order (judgment) for an unpaid amount, interest will continue to be charged on that court-ordered amount daily, using the same rate, until you pay the entire debt, unless the court says otherwise.

6. FEES AND CHARGES

6.1. You must pay us all fees and charges listed in the Schedule, any required government transaction charges, and any other fees, including costs we spend to enforce the contract, at the times specified.

6.2. Even if you don't accept the loan offer or the contract ends, we can still keep or charge you for any fees and charges we have already paid to third parties.

7. SECURITY

7.1. This loan is unsecured (no property is used as collateral).

8. DEFAULT (Breaking the Contract)

8.1. These are "Default Events" (when you break the contract): a) You fail to make any payment on time or in full. b) You break any promise or warranty you gave us. c) We reasonably believe you tricked us (fraud) into giving you the loan. d) You die, lose your full legal ability (capacity), or try to declare bankruptcy or arrange debt relief with creditors. e) You don't tell us in writing that you changed your address, and we can't find you after trying reasonably hard. f) You break the terms of an insurance policy, fail to renew one that we both agreed on, or the insurer cancels a policy we asked for. g) Property used as security (if applicable) is taken out of your control. h) A court order is used against the secured property (if applicable).

8.2. Waiver for First Missed Payment: a) Even if you miss a payment or a payment is rejected (dishonored) (but not because you stopped it), we may choose not to treat it as a formal Default Event (at our choice). b) If a payment by direct debit is rejected for the first time, we must send you a special Direct Debit Default Notice, but we will not count it as a regular Default Notice.

8.3. Default Interest Rate: If the contract's Financial Table lists a default interest rate, that rate may be charged on the amount you failed to pay. If no default rate is listed, the original interest rate still applies.

8.4. Enforcement Costs: If you default, you must pay all reasonable costs we spend to enforce our rights under the contract.

8.5. You must pay all reasonable enforcement costs we spend because of your default. We will try to keep these costs low, but your actions (like not telling us your new address) could cause extra costs.

8.6. Default Notice Process: If you are in default, we will send you a Default Notice that will tell you: a) What you did wrong (the default). b) What you need to do to fix it (remedy). c) How much time you have to fix it (at least 30 days). If you can't fix it in time, tell us immediately so we can try to help you.

8.7. If you fix the default within the time given, we will not take any further action.

8.8. If you ignore the Default Notice: a) We can immediately declare that all money you owe is due right away and/or start taking legal action, without giving you further notice (we must still follow all laws). b) If your late payments (arrears) are unpaid for more than 60 days and: i. We can't contact you using the last address or contact information you gave us; or ii. You don't reply to our communication/letters/notices; or iii. You don't fix the late payment; or iv. You don't try to discuss delaying enforcement action; We may list you as a defaulter with a Credit Reporting Body. WARNING: This could make getting credit harder in the future.

8.9. Our Right to Act: If you fail to do anything required by the contract, any mortgage, or any insurance policy, we may act as if we were the owner to protect our interests: a) Do whatever is needed. b) Do it using your name. c) Do it at your cost, and charge the expense to your account. These costs will be treated as enforcement expenses.

8.10. Our Rights After Default (Subject to Law): After a default, we can: a) Use any power this contract or the law gives us, including selling any secured property. b) Pay off any money owed to others on the secured property to protect our interests. This amount becomes an enforcement expense and is added to your total debt. c) Appoint agents or receivers to manage all or part of the secured property. d) Pay off and take over or clear any other mortgage on the secured property. e) Perform any of your duties under this contract.

8.11. You Must Cover Our Losses: To the maximum extent allowed by law, you must pay us back for all losses, enforcement costs, or damages we suffer because you broke or refused to follow this loan contract.

9. Delaying Action (Postponement), Including Due to Hardship

9.1. If we have sent you a Default Notice (a warning that you broke the contract) and: a) The default can be fixed (for example, if you can't pay all the overdue amounts yet); AND b) You haven't claimed hardship yet and haven't failed to fix the same type of default before the deadline we gave you; AND c) The reason for your default is something serious like illness, unemployment, family violence, or another good reason; You may ask us to delay any enforcement action (like demanding full payment) because of this hardship or for other reasons.

9.2. We will tell you our decision in writing. Any delay is completely up to us (at our discretion) and will have terms and conditions that we believe are fair.

10. Statements

10.1. Unless the National Credit Code says otherwise, we will send you a Statement of Account for your loan at least every six months (or more often if we decide). You can ask for an extra statement at any time, but you may have to pay a fee if one is listed in the Schedule.

11. Payments

11.1. You must pay us the total balance and all other amounts you owe under the loan contract according to the Schedule. On the final repayment date, or when the full balance is due (whichever is later), you must pay us everything you owe.

11.2. As far as the law allows, you must make all payments without deducting any amounts you think we owe you (no set-off or counterclaim).

11.3. Your payment is officially credited to your account on the date we receive it, the date shown on the bank statement, or the date the money is taken from your account (if paying by direct debit).

11.4. Any money we get from using our rights (e.g., selling secured property) will be used to pay your total debt, and must be applied in this order (unless the law requires otherwise): a) Pay all the costs and expenses we spent using our rights. b) Pay the total amount you owe us. c) Pay you the remaining balance (if any). This remaining amount does not earn interest.

11.5. We may hold an amount of money equal to any part of your total debt that is not yet due for payment and credit it to your account. If you ask, we may refund it.

11.6. If a payment is rejected (dishonored) or if we have to refund money to a bankruptcy trustee, liquidator, or bank (due to a disputed charge), the money will be treated as if we never received it. This means we get back all our rights against you under the contract.

12. Our Changes

12.1. We can change the terms of our offer at any time before you sign it. If we do, we will let you know.

12.2. After you sign, if we find it necessary, we can change some of the contract terms or how it works without your permission. If we do, we will notify you at least 21 days before the change starts. The changes we can make are: a) Changing the amount or frequency of repayments. b) Changing how interest is calculated or applied (if we change our software system). c) Changing the amount or frequency of fees and charges. d) Adding new fees and charges. e) Changing how the reference interest rate is published (if applicable). If you disagree with these changes, you may end the contract and pay off your loan without any penalty before the change takes effect.

12.3. Once the contract is signed and the loan is given, the interest rate will be fixed for the loan term (unless changed under clause 12.2).

12.4. If a default happens and the missed payment plus any related fees are not paid before the expected maturity date, we may extend your loan maturity by continuing to take the same repayment amount until the total debt is paid off.

12.5. We will only change a repayment amount or date after the loan is signed: at your request, by an agreement we make with you, or by notifying you. If we notify you of a change and you cannot make the payment on the new date or amount, you must tell us right away so we can try to help you.

13. Notices

13.1. We can send you any notice in any legal way, including delivering it in person or mailing it to any address you gave us, even if you don't live there anymore. We will only send notices electronically if you have told us a method we can use, and only for documents the National Credit Code allows.

13.2. Any notice will be delivered to you according to the National Credit Code rules.

13.3. If two or more of you are borrowers, you can choose one person to receive notices for everyone. If you do this, a notice sent to that chosen person is considered received by all of you.

13.4. You must tell us as soon as possible if you change your name or contact details.

13.5. You can send us notices by handing them to an employee at our office, by pre-paid mail, or by electronic means. We will notify you if we change our contact details.

13.6. We won't consider a notice or document received if you addressed it incorrectly or used an inactive or invalid electronic method.

14. Transferring the Contract (Assignment)

14.1. You cannot sell, transfer, or deal with your rights under this loan contract without our permission.

14.2. We can sell or transfer (assign) this loan contract if we need to. a) You must sign any documents and do anything else we reasonably ask to help us transfer the contract. b) Transferring the contract does not change your obligations to us. c) If we plan to sell your loan, we will notify you in writing and give you the option to pay off the loan or find other financing within a reasonable time.

14.3. When transferring the loan, if necessary and legal, we can share any information about you and this contract with the relevant person.

15. Insurance

15.1. No insurance is required under this loan contract.

16. Disputes

16.1. If you have a dispute or are unhappy with our actions, you agree to follow these steps: * Step 1 (First Contact): Call us at 0480 160 462 and explain your problem. We can usually fix issues quickly and informally. (Note: This first call is not the formal Internal Dispute Resolution process). * Step 2 (Formal Complaint): If you're not satisfied, you must contact our Internal Dispute Resolution (IDR) Manager, Mahesh Pant, at (04) 3076 1830 as soon as possible. We may ask you to submit your complaint in writing (email or post) for further investigation. * Step 3 (External Review): If you are still unsatisfied after using both Steps 1 and 2, you can contact the Australian Financial Complaints Authority (AFCA). * Contact AFCA: Write to GPO Box 3, Melbourne Victoria 3001, call 1800 931 678, email info@afca.org.au, or visit their website. * Important: You must go through our IDR process first. If you don't, AFCA will send the matter back to us to resolve initially.

17. Trusts

17.1. If you are the Trustee of any Trust (whether you told us or not), you promise that: a) You are personally liable and liable as the Trustee if the loan benefits the Trust. b) Entering into this loan as a Trustee is commercially beneficial for the Trust. c) You have the full authority to enter into this contract as the Trustee for a proper purpose. d) You are acting in a way that allows us (the Lender) to use the Trust's assets to cover liabilities from the loan.

17.2. You must get our permission before you: a) Change the Trustee of the Trust; b) End (terminate) the Trust; or c) Change the terms of the Trust Deed.

17.3. You agree to: a) Follow the Trust Deed and ensure the Trust continues and operates correctly. b) Perform your duties as Trustee carefully to ensure the Trust's obligations under this guarantee are met.

18. General Matters

18.1. The Agreement: a) This loan contract contains the complete agreement between us about the loan. It can be signed in multiple copies (counterparts), and all copies together form the single contract. This contract follows all legal rights you or we may have and any future written agreements between us. b) This contract cannot be changed unless the change is in writing and signed by all parties (you and us). c) If there is more than one borrower, this contract applies to and binds each of you individually and all of you as a group.

18.2. Conflict Resolution: If there is any difference between the Schedule and these General Conditions, the details in the Schedule will be used, unless there is an obvious mistake.

18.3. Reliance on Our Certification: We will rely on any written notice or certificate signed by or for us as proof of: a) A default has happened under this contract; and b) The amount you owe and must pay under this contract. This will be considered correct unless you can prove we made a mistake, or a court or external dispute body decides otherwise.

18.4. Your Obligations Continue: Your duties under this contract continue no matter what happens to you, the loan amount, or anything else. For example, your obligation to repay continues even if you die or become bankrupt.

18.5. Loan Discharge (Ending the Contract): a) If you ask us to formally end the loan contract (discharge), and we are not sure the loan is fully settled, we will give you a statement of the outstanding balance within one week. The loan will only be discharged after you fully pay this outstanding amount. b) We do not have to discharge the loan until we are certain that you are unlikely to owe us any more money (for example, if a final payment might be rejected or taken back). Even if the contract is discharged, any amount you still owe, or that becomes outstanding later, must still be paid.

18.6. Unenforceable Clauses: If any part of this contract is illegal, void, or cannot be enforced, we will read the contract as if that provision were changed as little as possible to make it legal and enforceable, or removed entirely if necessary.

19. Interpretation (Understanding the Terms)

19.1. Definitions: In your loan contract: * "account" means the account you hold with us for the loan. * "amount of credit provided" means the amount stated in the Financial Table of this contract. * "annual percentage rate" means the yearly rate described in the Schedule. * "arrears" means the difference between what your account balance actually is and what it should be if you had made all payments on time. * "balance" means the difference between all money added (credited) and all money taken out (debited) from your account. * "business day" means any day except Saturday, Sunday, or a national public holiday. * "credit fees and charges" means the fees and charges listed in the Schedule (as defined in the National Credit Code). * "credit provider" means Support Finance Pty Ltd. * "daily balance" means the balance at the end of a day. * "disclosure date" means the date mentioned in the Schedule. * "EDR" means the process used by our approved External Dispute Resolution scheme provider. * "electronic address" means the email, fax, or mobile number you have given us permission to use for contact. * "General Conditions" means this entire document of General Conditions. * "government transaction charges" means government charges or duties on receipts or withdrawals related to your loan (like stamp duty), whether you are primarily responsible for paying them or not. * "IDR" means our Internal Dispute Resolution process. (You must use this before contacting EDR). * "law" means all common law and legal principles, including legislation. * "legislation" means any laws, rules, or regulations passed by any government authority (including amendments). * "loan" means the credit we have given or will give you under this contract. * "loan contract" means this entire agreement once both you and we have signed it. * "National Credit Code" means Schedule 1 of the National Consumer Credit Protection Act 2009. * "party" means either you or us. * "Schedule" means the Schedule attached to your loan contract. * "Settlement date" means the date the loan (or part of it) is first charged to your account. * "State" means any State or Territory of Australia. * "total amount owing" means all money you owe us under this loan contract or any other agreement, including enforcement expenses (but excludes amounts prohibited by the National Credit Code). * "us", "our", and "we" means Support Finance Pty Ltd. * "you" means each borrower named in the Schedule.

19.2. General Rules for Reading the Contract: a) Headings are for convenience only and don't affect the meaning of the contract. b) Words that mean one thing (singular) also include many things (plural), and vice-versa. c) A reference to a person includes an individual and a company. d) References to a document include all its later changes or replacements. e) Words used here have the same meaning as in the Schedule and the National Credit Code. f) References to any person (including you or us) include their successors or legal representatives.

19.3. The word "includes" is used as an example and does not limit the definition of the term it applies to.

THE BALANCE OF THIS PAGE IS INTENTIONALLY BLANK

In Nepali

ऋण सम्झौताका सामान्य शर्तहरू

१. ऋण रकम उपलब्ध गराउनु अघि पूरा गर्नुपर्ने शर्तहरू

हामीले तपाईंलाई ऋण रकम तब मात्र दिनेछौं जब निम्न सबै शर्तहरू पूरा हुन्छन्:

१.१. ऋण पाउनका लागि, तपाईंले:

क) आफ्नो पहिचान सन्तोषजनक रूपमा प्रमाणित गर्नुपर्छ, जसले हामीलाई सबै सरकारी/कानुनी आवश्यकताहरू पूरा गर्न मद्दत गर्दछ।

ख) तपाईंको आवश्यकताको आधारमा यो ऋण अनुपयुक्त छैन भन्ने कुरामा हामी सन्तुष्ट हुनुपर्छ।

ग) तपाईंले ऋणको किस्ता ठूलो आर्थिक कठिनाइबिना तिर्न सक्ने क्षमता देखाउनुपर्छ। यो जानकारी तपाईं आफैंले वा तपाईंको तर्फबाट कसैले दिएको हुन सक्छ।

घ) हामीलाई आवश्यक लागेमा, हाम्रो क्रेडिट रिपोर्टिङ एजेन्सीबाट सन्तोषजनक क्रेडिट रिपोर्ट प्राप्त गर्नुपर्छ।

ङ) हामीले मागेका सबै कागजात, सामग्री वा जानकारी हामीले प्राप्त गर्नुपर्छ र ती कुराहरूमा हामी सन्तुष्ट हुनुपर्छ।

च) हाल तपाईंले अन्य ऋणदाताहरूबाट लिएका सबै ऋणहरूको बारेमा सत्य जानकारी दिनुभएको छ भन्ने कुरामा हामीलाई विश्वस्त पार्नुपर्छ।

छ) तपाईंले आवेदन गर्दा दिनुभएका सबै बयान तथा ग्यारेन्टीहरू सत्य, सही र भ्रमपूर्ण छैनन् भन्ने कुरामा हामीलाई विश्वस्त पार्नुपर्छ।

ज) तपाईंले यो ऋण सम्झौतामा सही गरेर हाम्रो प्रस्ताव स्वीकार गर्नुपर्छ।

झ) तपाई हामीले बीचको सम्झौतामा सही गर्नुपर्छ।

१.२. ऋण सम्बन्धी छलफल:

तीस (३०) दिनभित्र तपाईं वा तपाईंको तर्फबाट कसैले पनि कुनै लेखापाल, वित्तीय सल्लाहकार, योजनाकार वा कुनै पनि ऋण मिनाहा वा राहत, वा कुनै प्रकारको दिवालियापन (bankruptcy) सम्बन्धी सम्झौता गर्ने व्यवसायसँग सम्पर्क वा छलफल गर्नुभएको छैन भन्ने कुरा तपाईले स्वीकार गर्नु पर्छ। यदि गर्नुभएको छ भने, हामीले ऋण उपलब्ध गराउनुअघि नै तपाईंले हामीलाई भन्नुपर्छ।

१.३. सम्झौतामा सही गर्नुअघि ऋण रद्द गर्ने कारणहरू:

यदि हामीले सम्झौतामा सही गर्नुअघि कुनै पनि समयमा:

क) तपाईंको आर्थिक अवस्थालाई असर गर्न सक्ने कुनै घटना वा परिस्थिति उत्पन्न भयो भने, वा

ख) तपाईंले जानकारी लुकाएको वा ऋण स्वीकृतिका लागि महत्त्वपूर्ण हुन सक्ने कुनै पनि अवस्थाको बारेमा हामीलाई थाहा भयो भने, हामी ऋण दिन अस्वीकार गर्नेछौं।

यदि हामीले यसो गर्यौं भने, तपाईंले बेहोर्नुपरेको कुनै पनि हानि वा लागतको लागि हामी जिम्मेवार हुने छैनौं।

१.४. सरकारी शुल्क वृद्धि:

यदि ऋण उपलब्ध गराउनुअघि तालिकामा तोकिएका कुनै सरकारी शुल्क वा चार्ज बढेमा, तपाईले बढेको शुल्क तिर्ने गरी सम्झौता परिवर्तन गर्न सहमत नभएसम्म हामीले ऋण रकम उपलब्ध गराउन आवश्यक हुने छैन।

२. ऋण

२.१. हामी तपाईंको आवेदनमा उल्लेख गरिएको उद्देश्यको लागि ऋण उपलब्ध गराउन सहमत छौं।

३. पुनः निकाल्ने सुविधा (Redraw Facility)

३.१. यो ऋण सम्झौता अन्तर्गत पुनः पैसा निकाल्ने वा थप ऋण लिने सुविधा उपलब्ध छैन।

४. खाता र भुक्तानी

४.१. हामी तपाईंको ऋण सम्झौता अन्तर्गत दिइएको ऋण रकम र सम्झौताले हामीलाई डेबिट गर्न अनुमति दिएका अन्य सबै कुराहरू तपाईंको खातामा चार्ज गर्न सक्छौं।

५. ब्याजको गणना र चार्ज

५.१. ब्याज दर: यो ऋणमा लागू हुने वार्षिक ब्याज दर ३५.७५ युएस डलर हुनेछ।

* वार्षिक दरलाई ३६५ ले भाग गरेर दैनिक प्रतिशत दर निकालिन्छ।

* ब्याज दैनिक रूपमा (९ दशमलव स्थानसम्म) तपाईंको दैनिक ब्यालेन्समा लागू हुने दर प्रयोग गरी गणना गरिन्छ।

* प्रत्येक दिनको ब्याज जम्मा गरिन्छ (चक्रवृद्धि हुँदैन) र कुल ब्याज प्रत्येक महिनाको अन्तिम दिनमा (२ दशमलव स्थानमा राउन्ड गरेर) तपाईंको खातामा चार्ज गरिन्छ।

* तपाईंले पूरा ऋण तिरेको दिनमा पनि हामी ब्याज चार्ज गर्नेछौं।

५.२. जब हामी तपाईंको खातामा कुनै ब्याज चार्ज गर्छौं, त्यो रकम पनि ब्याज गणना हुने ब्यालेन्सको हिस्सा बन्छ।

५.३. यदि तपाईंले तिर्न बाँकी रकमको लागि हामीले अदालतबाट आदेश (फैसला) प्राप्त गर्यौं भने, अदालत वा न्यायाधिकरणले अन्यथा निर्धारण नगरेसम्म, तपाईंले पूर्ण ऋण नतिरुन्जेलसम्म सो फैसला गरिएको रकममा दैनिक दर लागू गरेर ब्याज गणना भइरहन्छ।

६. शुल्क र चार्ज

६.१. तपाईंले तालिकामा तोकिएका क्रेडिट शुल्क र चार्जहरू, लागू भएमा सरकारी कारोबार शुल्कहरू र सम्झौता अन्तर्गत लाग्न सक्ने अन्य शुल्क वा खर्चहरू (कार्यान्वयन खर्चहरू सहित) तिर्नुपर्छ।

६.२. तपाईंले ऋण सम्झौता स्वीकार नगरे तापनि वा यो सम्झौता कुनै कारणले समाप्त भए तापनि, हामीले तेस्रो पक्षहरूलाई भुक्तानी गरिसकेका क्रेडिट शुल्क र चार्जहरू राख्न वा भुक्तानीको लागि माग गर्न सक्छौं।

७. धितो

७.१. यो ऋण धितो (Unsecured) रहित छ।

८. शर्त उल्लंघन र पूर्वनिर्धारित घटनाहरू (Default and Events of Default)

८.१. निम्न घटनाहरूलाई शर्त उल्लंघन (Default Events) मानिनेछ:

क) तपाईंले नियत मितिमा सम्पूर्ण वा कुनै पनि किस्ता रकम तिर्न असफल हुनुभयो।

ख) तपाईंले हामीलाई दिनुभएको कुनै पनि वाचा वा ग्यारेन्टी तोड्नुभयो।

ग) हामीले तपाईंले धोका दिएर (fraud) ऋण सम्झौतामा प्रवेश गरेको विश्वास गर्ने उचित आधार पायौं।

घ) तपाईंको मृत्यु भयो वा तपाईंले पूर्ण कानुनी क्षमता गुमाउनुभयो वा तपाईं दिवालियापन घोषणा गर्ने प्रयास गर्नुहुन्छ।

ङ) तपाईंले आफ्नो ठेगाना परिवर्तन भएको जानकारी लिखित रूपमा दिन असफल हुनुभयो र हामीले उचित प्रयास गरेपछि पनि तपाईंलाई भेट्टाउन सकेनौं।

च) तपाईंले कुनै बीमा नीतिको शर्त तोड्नुभयो वा हामीलाई सन्तुष्ट पार्ने गरी बीमा नवीकरण गर्न असफल हुनुभयो वा हामीले मागेको बीमा रद्द भयो।

छ) धितो राखिएको सम्पत्ति कुनै पनि तरिकाले तपाईंको नियन्त्रणबाट बाहिर गयो। (लागू भएमा)

ज) धितो राखिएको सम्पत्ति वा त्यसबाट प्राप्त आम्दानी विरुद्ध कुनै अदालतको आदेश लागू गरियो। (लागू भएमा)

८.२. पहिलो भुक्तानी छुटको नियम:

क) माथि ८.१(क) मा उल्लेख भए तापनि, यदि तपाईंले नियत मितिमा कुनै रकम तिर्नुभएन वा तपाईंले भुक्तानी रद्द नगर्दा पनि भुक्तानी अस्वीकृत (dishonor) भयो भने, हामीले आफ्नो विवेकमा त्यसलाई शर्त उल्लंघन नमान्ने निर्णय गर्न सक्छौं।

ख) यदि तपाईंको पहिलो डाइरेक्ट डेबिट भुक्तानी अस्वीकृत भयो भने, हामीले तपाईंलाई कानुनी डाइरेक्ट डेबिट डिफल्ट नोटिस दिनुपर्छ, तर हामी यसलाई 'शर्त उल्लंघन नोटिस' को रूपमा लिने छैनौं।

८.३. ब्याजको पूर्वनिर्धारित दर:

यदि यस सम्झौताको वित्तीय तालिकामा 'पूर्वनिर्धारित ब्याज दर' उल्लेख छ भने, तपाईंले भुक्तानी गर्न बाँकी रहेको रकममा सो दर लागू हुन सक्छ। यदि कुनै दर उल्लेख गरिएको छैन भने, पूर्वनिर्धारित दर लागू हुँदैन, तर ब्याज तालिकामा तोकिएको दरमा लागु भइरहनेछ।

८.४. तपाईंको शर्त उल्लंघनको अवस्थामा कार्यान्वयन खर्चहरू लाग्न सक्छन् र तपाईंको खातामा चार्ज हुन सक्छन्।

८.५. तपाईंको शर्त उल्लंघनको कारणले हाम्रो अधिकार प्रयोग गर्न लाग्ने सबै उचित कार्यान्वयन खर्चहरू तपाईंले हामीलाई तिर्नुपर्नेछ। यी खर्चहरू कम गर्न हामी प्रयास गर्नेछौं, तर तपाईंको कार्यहरू (जस्तै नयाँ ठेगाना नबताउनु) ले हामीलाई थप कारबाही गर्न बाध्य पारेमा अतिरिक्त लागत लाग्न सक्छ।

८.६. शर्त उल्लंघन सूचना (Default Notice):

यदि तपाईं शर्त उल्लंघनको अवस्थामा हुनुहुन्छ भने, हामी तपाईंलाई एक सूचना पठाउनेछौं, जसमा:

क) तपाईंको गल्ती के हो;

ख) गल्ती सुधार्न तपाईंले के गर्नुपर्छ;

ग) गल्ती सुधार्नका लागि दिइने समय (सूचना दिएको मितिबाट कम्तीमा ३० दिन) उल्लेख गरिनेछ।

यदि तपाईं तोकिएको समयभित्र गल्ती सुधार्न सक्नुहुन्न भने, हामीलाई सहयोगको लागि तुरुन्तै जानकारी दिनुहोस्।

८.७. यदि तपाईंले तोकिएको समयभित्र सूचनामा भनिएका कुराहरू पूरा गर्नुभयो भने, हामी यो ऋण सम्झौता अन्तर्गत कुनै कारबाही गर्ने छैनौं।

८.८. यदि तपाईंले शर्त उल्लंघन सूचनाको पालना गर्नुभएन भने:

क) हामी, हाम्रा कर्मचारीहरू वा एजेन्टहरूले कानुनी आवश्यकताहरूको अधीनमा रही तपाईंले तिर्न बाँकी रहेको सबै रकम तुरुन्तै तिर्नुपर्नेछ भनी निर्णय गर्न सक्छौं वा थप सूचना बिना कार्यान्वयन कारबाही सुरु गर्न सक्छौं।

ख) यदि तपाईंको बाँकी बक्यौता ६० दिनभन्दा बढी भयो र:

i. हामीले तपाईंले दिनुभएको अन्तिम ठेगाना वा अन्य सम्पर्क माध्यमबाट तपाईंलाई सम्पर्क गर्न सकेनौं; वा

ii. तपाईंले हामीले दिएको कुनै पनि सूचना/पत्रको जवाफ दिन असफल हुनुभयो; वा

iii. तपाईंले बक्यौता रकम तिर्न असफल हुनुभयो; वा

iv. तपाईंले कार्यान्वयन कारबाही स्थगित गर्न वार्ता गर्न असफल हुनुभयो;

हामी तपाईंलाई क्रेडिट रिपोर्टिङ निकायमा 'डिफल्टर' को रूपमा सूचीकृत गर्न सक्छौं।

चेतावनी: यसले भविष्यमा ऋण प्राप्त गर्न कठिन बनाउन सक्छ।

८.९. यदि तपाईंले यो ऋण सम्झौता वा कुनै बीमा नीति अनुसार गर्नुपर्ने कुनै पनि काम गर्न असफल हुनुभयो भने, हामी हाम्रो हितको रक्षा गर्न सम्पत्तिको मालिकजस्तै व्यवहार गरेर निम्न कार्य गर्न सक्छौं:

क) आवश्यक पर्ने जुनसुकै काम गर्ने;

ख) तपाईंको नाममा गर्ने;

ग) तपाईंको खर्चमा गर्ने र सो खर्च तपाईंको खातामा चार्ज गर्ने।

यसो गर्दा लाग्ने कुनै पनि खर्चलाई कार्यान्वयन खर्च मानिनेछ।

८.१०. शर्त उल्लंघनपछि हाम्रा अधिकारहरू (कानूनको अधीनमा):

शर्त उल्लंघनको घटनापछि, हामी निम्न कार्यहरू गर्न सक्छौं:

क) यस ऋण सम्झौताले दिएको कुनै पनि अधिकार प्रयोग गर्ने, जसमा धितो राखिएको सम्पत्ति बेच्ने वा कसैलाई खरिद गर्ने विकल्प दिने समावेश छ।

ख) हाम्रो हितको रक्षा गर्न धितो राखिएको सम्पत्ति सम्बन्धी कसैलाई तिर्नुपर्ने पैसा तिर्ने। यो रकम कार्यान्वयन खर्च हुनेछ र कुल ऋण रकमको हिस्सा बन्नेछ।

ग) धितो राखिएको सम्पत्तिको व्यवस्थापन गर्न एजेन्ट वा रिसीभरहरू नियुक्त गर्ने।

घ) धितो राखिएको सम्पत्तिमा असर पार्ने अन्य कुनै धितो वा चार्ज तिर्ने र त्यसको स्थानान्तरण वा निस्कासन प्राप्त गर्ने।

ङ) यस ऋण सम्झौता अन्तर्गत तपाईंको कुनै पनि दायित्वहरू पूरा गर्ने।

८.११. कानूनले अनुमति दिएको अधिकतम हदसम्म, तपाईंले यो ऋण सम्झौता उल्लंघन गरेको कारणले हामीले बेहोरेका सबै नोक्सान, कार्यान्वयन खर्च वा लागतहरू हामीलाई तिर्नुपर्छ।

९ कठिनाइ सहितका कारणले कार्यान्वयन कारबाही स्थगित गर्ने

९.१. यदि हामीले तपाईंलाई शर्त उल्लंघन सूचना (Default Notice) जारी गरेका छौं र: क) उक्त उल्लंघन सुधार्न सकिने प्रकारको छ (जस्तै: बक्यौताको सम्पूर्ण रकम तिर्न नसक्नु); र ख) तपाईंले हामीलाई पहिले कठिनाइको दाबी गर्नुभएको छैन र तोकिएको म्यादभित्र सोही प्रकृतिको अर्को उल्लंघन गर्नुभएको छैन; र ग) तपाईंको शर्त उल्लंघनको कारण बिरामी, बेरोजगारी, पारिवारिक हिंसा वा अन्य उचित कारण हो; तपाईंले कठिनाइ वा अन्य कारणले कुनै पनि कार्यान्वयन कारबाही स्थगित गर्न अनुरोध गर्न सक्नुहुन्छ।

९.२. हामी तपाईंलाई आफ्नो निर्णय लिखित रूपमा जानकारी दिनेछौं। कुनै पनि स्थगन हाम्रो विवेकमा निर्भर हुनेछ र हामीले उचित ठानेका नियम र शर्तहरूमा आधारित हुनेछ।

१०. विवरणहरू (Statements)

१०.१. राष्ट्रिय ऋण संहिता (National Credit Code) ले नमागेसम्म, हामी तपाईंलाई हरेक ६ महिनामा (वा हामीले निर्णय गरेमा छोटो अन्तरालमा) ऋण खाताको विवरण (Statement of Account) उपलब्ध गराउनेछौं। तपाईंले जुनसुकै बेला थप विवरण अनुरोध गर्न सक्नुहुन्छ, तर शुल्क र चार्जको तालिकामा उल्लेख गरिएको भए शुल्क लाग्न सक्छ।

११. भुक्तानीहरू

११.१. तपाईंले तालिका अनुसार ऋण सम्झौता अन्तर्गत तिर्नुपर्ने बक्यौता र अन्य सबै रकमहरू हामीलाई तिर्नु बुझाउनुपर्छ।अन्तिम किस्ताको मिति वा ऋण सम्झौताको बाँकी बक्यौता तिर्नुपर्ने दिन (जुनपछि हुन्छ) मा, तपाईंले खाताको सम्पूर्ण बक्यौता र तपाईंले हामीलाई तिर्न बाँकी अन्य सबै रकमहरू (यदि छन् भने) चुक्ता गर्नुपर्छ।

११.२. कानुनले अनुमति दिएसम्म, ऋण सम्झौता अन्तर्गतका सबै भुक्तानीहरू कुनै पनि कट्टी (set-off) वा प्रतिदाबी (counterclaim) बिना हुनुपर्छ।

११.३. तपाईंको भुक्तानी हामीले प्राप्त गरेको मिति, बैंक स्टेटमेन्टमा देखाइएको मिति, वा (डाइरेक्ट डेबिट भुक्तानीको हकमा) पैसा निकालिएको मितिमा मात्र तपाईंको खातामा जम्मा हुनेछ।

११.४. यस ऋण सम्झौता अन्तर्गत हामीले आफ्नो अधिकार प्रयोग गरेर प्राप्त गरेको कुनै पनि रकम तपाईंले तिर्नुपर्ने कुल रकम तिर्न प्रयोग गर्न सकिन्छ, र कानुनले अन्यथा नमागेसम्म, निम्न क्रममा लागू गरिनेछ: क) यस ऋण सम्झौता अन्तर्गत हाम्रो अधिकार प्रयोग गर्दा लागेका सबै लागत र खर्चहरू तिर्न। ख) हामीलाई तिर्नुपर्ने कुल रकम तिर्न। ग) बाँकी रकम (यदि छ भने), जसमा ब्याज लाग्दैन, तपाईंलाई फिर्ता गर्न।

११.५. राष्ट्रिय ऋण संहिताका प्रावधानहरूको अधीनमा रहेर, हामीले त्यतिबेला भुक्तानी गर्न बाँकी नरहेको कुल ऋण रकम बराबरको पैसा राख्न सक्छौं र त्यसलाई तपाईंको खातामा जम्मा गर्न सक्छौं, वा तपाईंले अनुरोध गरेमा फिर्ता गर्न सक्छौं।

११.६. यदि कुनै भुक्तानी अस्वीकृत भयो (dishonored) वा कुनै दिवालियापनको ट्रस्टी वा बैंकलाई पैसा फिर्ता गर्न हामी बाध्य भयौं भने, सो रकम कहिल्यै प्राप्त नभएको मानिनेछ र हामीले तपाईं विरुद्ध यस ऋण सम्झौता अन्तर्गतका सबै अधिकारहरू पुन: प्राप्त गर्नेछौं।

१२. हाम्रो परिवर्तनहरू

१२.१. तपाईंले ऋण सम्झौता स्वीकार गर्नुअघि हामीले आफ्नो प्रस्तावका शर्तहरू कुनै पनि बेला परिवर्तन गर्न सक्छौं। यसो गरेमा, हामी तपाईंलाई जानकारी दिनेछौं।

१२.२. तपाईंले हस्ताक्षर गरेपछि पनि, हामीले आवश्यक ठानेमा तपाईंको सहमतिबिना ऋण सम्झौताका केही शर्तहरू वा यसको सञ्चालन गर्ने तरिका परिवर्तन गर्न सक्छौं। यसो गरेमा, हामीले प्रस्तावित परिवर्तन लागू हुनुभन्दा कम्तीमा २१ दिन पहिले तपाईंलाई सूचित गर्नेछौं। हामीले गर्न सक्ने परिवर्तनहरू: क) किस्ता भुक्तानीको रकम वा आवृत्ति (कति पटक तिर्ने) मा परिवर्तन। ख) हाम्रो सफ्टवेयर प्रणाली परिवर्तन भएमा, ऋणमा ब्याज गणना वा लागू गर्ने तरिकामा परिवर्तन। ग) शुल्क र चार्जहरूको रकम वा आवृत्ति मा परिवर्तन। घ) नयाँ शुल्क र चार्जहरू लागू गर्ने। ङ) सन्दर्भ दर (reference rate) प्रकाशन गर्ने विधिमा परिवर्तन (लागू भएमा)। यदि तपाईं यी परिवर्तनहरूसँग असहमत हुनुहुन्छ भने, परिवर्तन लागू हुनुअघि कुनै दण्डबिना सम्झौता समाप्त गरी ऋण चुक्ता गर्न सक्नुहुन्छ।

१२.३. एकपटक यो सम्झौता हस्ताक्षर भई ऋण रकम दिइसकेपछि, ब्याज दर ऋण अवधिभरि स्थिर रहनेछ (धारा १२.२ को अधीनमा)।

१२.४. यदि ऋण अवधिमा शर्त उल्लंघन भयो र बक्यौता रकम तथा तालिकामा तोकिएका कुनै शुल्कहरू अपेक्षित परिपक्वता मिति (maturity date) अघि भुक्तानी गरिएन भने, हामीले तपाईंको ऋणको परिपक्वता अवधि बढाउन सक्छौं। कुल ऋण रकम चुक्ता नभएसम्म हामी त्यही रकम र आवृत्तिमा तपाईंको खाताबाट किस्ता काट्न जारी राख्नेछौं।

१२.५. एकपटक यो सम्झौता हस्ताक्षर भई ऋण रकम दिइसकेपछि, हामीले किस्ताको रकम वा मिति तपाईंको अनुरोधमा, आपसी वार्ताको माध्यमबाट वा तपाईंलाई हामीले सूचना दिएर मात्र परिवर्तन गर्नेछौं। यदि हामीले सूचना दियौं र तपाईं नयाँ रकम वा मितिमा भुक्तानी गर्न असमर्थ हुनुभयो भने, तपाईले हामीलाई तुरुन्तै जानकारी दिनुपर्छ ताकि हामी तपाईंलाई सहयोग गर्ने प्रयास गर्न सकौं।

१३. सूचनाहरू (Notices)

१३.१. हामीले तपाईलाई कानुनले अनुमति दिएको कुनै पनि तरिकाले सूचना वा अन्य कागजात पठाउन सक्छौं, जसमा व्यक्तिगत रूपमा बुझाउने वा तपाईंले हामीलाई उपलब्ध गराएको कुनै पनि ठेगानामा (हालको आवास नभए पनि) पठाउने समावेश छ। तपाईंले प्राविधिक विधि (electronic means) तोक्नुभएको खण्डमा र राष्ट्रिय ऋण संहिताले अनुमति दिएका कागजातहरू मात्र हामी विद्युतीय माध्यमबाट पठाउनेछौं।

१३.२. कुनै पनि सूचना वा अन्य कागजात राष्ट्रिय ऋण संहिताको आवश्यकता अनुसार तपाईंलाई डेलिभर गरिनेछ।

१३.३. कानुनले अनुमति दिएको हदसम्म, दुई वा दुईभन्दा बढी ऋण लिने व्यक्तिहरूले आफ्नो तर्फबाट सूचना र कागजातहरू प्राप्त गर्न एक जनालाई मनोनयन गर्न सक्नुहुन्छ। यसो गरेमा, मनोनित व्यक्तिलाई दिइएको सूचना सबैलाई दिइएको मानिनेछ।

१३.४. नाम वा सम्पर्क विवरण परिवर्तन भएमा वा परिवर्तन गर्ने मनसाय भएमा तपाईंले जतिसक्दो चाँडो हामीलाई सूचित गर्नुपर्छ।

१३.५. तपाईंले हामीलाई सूचना वा कागजातहरू हाम्रो कर्मचारीलाई व्यक्तिगत रूपमा बुझाएर, प्रिपेड हुलाक मार्फत हाम्रो हुलाक ठेगानामा पठाएर वा विद्युतीय माध्यम बाट दिन सक्नुहुन्छ। यदि हामीले हाम्रो ठेगाना वा सम्पर्क विवरण परिवर्तन गर्यौं भने, हामी तपाईंलाई सकेसम्म चाँडो सूचित गर्नेछौं।

१३.६. तपाईंले हामीलाई पठाएको कुनै पनि सूचना वा कागजात गलत ठेगानामा पठाउनुभयो वा निष्क्रिय वा अमान्य विद्युतीय विधि प्रयोग गर्नुभयो भने, हामीले त्यो प्राप्त गरेको मानिने छैन।

१४. सम्झौता हस्तान्तरण (Assignment)

१४.१. तपाईंले हाम्रो सहमतिबिना यो ऋण सम्झौता अन्तर्गतका आफ्ना अधिकारहरू हस्तान्तरण वा बेचबिखन गर्न सक्नुहुन्न।

१४.२. यदि हामीलाई आवश्यक लाग्यो भने हामीले यो ऋण सम्झौता हस्तान्तरण गर्न सक्छौं। क) तपाईंले ऋण सम्झौता हस्तान्तरण गर्न हामीलाई आवश्यक पर्ने सबै कागजातहरूमा सही गर्नुपर्छ र अन्य कामहरू गर्नुपर्छ। ख) सम्झौता हस्तान्तरण भए पनि तपाईंको दायित्वहरू परिवर्तन हुने छैनन्। ग) यदि हामी तपाईंको ऋण हस्तान्तरण गर्ने विचार गर्दैछौं भने, हामी तपाईंलाई लिखित रूपमा सूचना दिनेछौं र तपाईंलाई उचित अवधिभित्र ऋण चुक्ता गर्ने वा अन्य ठाउँबाट ऋण व्यवस्था गर्ने विकल्प प्रदान गर्नेछौं।

१४.३. यो ऋण सम्झौता हस्तान्तरण गर्ने हाम्रो अधिकार प्रयोग गर्दा, यो कानुनी र आवश्यक भएमा, हामीले तपाईं र यो ऋण सम्झौता सम्बन्धी कुनै पनि जानकारी सम्बन्धित व्यक्तिलाई दिन सक्छौं।

१५. बीमा

१५.१. यो ऋण सम्झौता अन्तर्गत कुनै बीमा आवश्यक छैन।

१६. विवादहरू (Disputes)

१६.१. हाम्रा कार्यहरूसँग विवाद वा असन्तुष्टि भएमा, तपाईं निम्न चरणहरू पछ्याउन सहमत हुनुहुन्छ: चरण १ (पहिलो सम्पर्क): ०४८० १६० ४६२ दिएको नम्बरमा हामीलाई सम्पर्क गर्नुहोस् र आफ्नो समस्या बताउनुहोस्। हामी सामान्यतया समस्याहरू तुरुन्तै र मैत्रीपूर्ण ढंगले समाधान गर्न सक्छौं। (नोट: यो सम्पर्क औपचारिक विवाद समाधान प्रक्रिया होइन)। चरण २ (आन्तरिक विवाद समाधान-IDR): यदि तपाईं हाम्रो प्रतिक्रियाबाट असन्तुष्ट हुनुहुन्छ भने, तपाईंले आन्तरिक विवाद समाधान (IDR) प्रबन्धक, महेश पन्तलाई (०४) ३०७६ १८३० मा जतिसक्दो चाँडो सम्पर्क गर्नुपर्छ। हामी थप अनुसन्धानको लागि तपाईंको उजुरी लिखित रूपमा (इमेल वा हुलाकबाट) माग्न सक्छौं। चरण ३ (बाह्य समीक्षा): यदि माथिका दुई चरणहरू प्रयोग गरेपछि पनि तपाईं हाम्रो IDR प्रक्रियाको नतिजाबाट सन्तुष्ट हुनुहुन्न भने, तपाईंले हाम्रो बाह्य विवाद समाधान योजना, अष्ट्रेलियन वित्तीय उजुरी प्राधिकरण (AFCA) लाई सम्पर्क गर्न सक्नुहुन्छ। AFCA सम्पर्क विवरण: GPO Box 3, Melbourne Victoria 3001 मा लेखेर, १८०० ९३१ ६७८ मा फोन गरेर, info@afca.org.au मा इमेल गरेर, वा उनीहरूको वेबसाइटमार्फत। महत्त्वपूर्ण: यसो गर्नुअघि तपाईंले पहिले हाम्रो IDR प्रक्रिया पूरा गरेको हुनुपर्छ। त्यसो गर्न सक्नु भएन भने, मामिला समाधानका लागि पहिले हामीलाई नै फिर्ता पठाइनेछ।

१७. ट्रस्टहरू

१७.१. यदि तपाईं कुनै पनि समयमा कुनै ट्रस्ट (Trust) को ट्रस्टी हुनुहुन्छ भने, तपाईं प्रतिज्ञा र ग्यारेन्टी दिनुहुन्छ कि: क) यदि ऋण सम्झौतामा प्रवेश गर्दा प्राप्त भएको कुनै पनि फाइदा ट्रस्टको हितमा छ भने, तपाईं व्यक्तिगत रूपमा र ट्रस्टीको क्षमतामा दुवै रूपमा यस ऋण सम्झौता अन्तर्गत जिम्मेवार हुनुहुन्छ। ख) ट्रस्टीको रूपमा यो ऋण सम्झौतामा प्रवेश गर्नु ट्रस्टको लागि व्यापारिक रूपमा लाभदायक छ। ग) ट्रस्टीको रूपमा यो ऋण सम्झौतामा प्रवेश गर्न तपाईंसँग पूर्ण अधिकार र शक्ति छ र तपाईंले उचित उद्देश्यका लागि यसो गरिरहनुभएको छ। घ) तपाईं यसरी कार्य गर्दै हुनुहुन्छ कि जसले ऋण सम्झौता अन्तर्गत लाग्ने दायित्वहरूको लागि ऋणदातालाई ट्रस्टको सम्पत्ति प्रयोग गर्न अनुमति दिन्छ।

१७.२. तपाईंले निम्न कार्यहरू गर्नुअघि हाम्रो सहमति लिनुपर्छ: क) ट्रस्टको ट्रस्टी परिवर्तन गर्न; ख) ट्रस्ट समाप्त गर्न; वा ग) ट्रस्ट डीड (Trust Deed) का शर्तहरू परिवर्तन गर्न।

१७.३. तपाईं सहमत हुनुहुन्छ कि: क) ट्रस्ट डीडका शर्तहरूको पालना गर्न र ट्रस्टको निरन्तरता र उचित सञ्चालन सुनिश्चित गर्न कार्य गर्न। ख) यस ग्यारेन्टी अन्तर्गत ट्रस्टका दायित्वहरू पूरा भएको सुनिश्चित गर्न उचित लगनशीलता र सावधानीका साथ ट्रस्टीको रूपमा आफ्नो दायित्वहरू पूरा गर्न।

१८. सामान्य कुराहरू (General Matters)

१८.१. सम्झौताको स्वरूप: क) यो ऋण सम्झौताले ऋण सम्बन्धी हामी र तपाईंबीचको सम्पूर्ण सहमति निर्धारण गर्दछ। यो सम्झौता जतिसुकै प्रतिहरूमा सही गरे पनि ती सबै मिलेर एउटै ऋण सम्झौता बन्नेछ। यो सम्झौता तपाईं वा हामीलाई कानुन अन्तर्गत प्राप्त सबै अधिकारहरू र भविष्यमा हामीबीच हुने कुनै पनि लिखित सम्झौताको अधीनमा रहनेछ। ख) यो ऋण सम्झौतामा परिवर्तन गर्नका लागि परिवर्तन लिखित रूपमा हुनुपर्छ र यस सम्झौताका सबै पक्षहरूले सही गरेको हुनुपर्छ। ग) यदि तपाईं एकभन्दा बढी हुनुहुन्छ भने, यो ऋण सम्झौता तपाईं प्रत्येकमा छुट्टाछुट्टै र तपाईं सबैमा सामूहिक रूपमा लागू हुन्छ र बाँध्छ।

१८.२. तालिका र शर्तहरू बीचको विवाद: यदि तालिका (Schedule) र यी सामान्य शर्तहरू (General Conditions) बीच कुनै विवाद वा असंगति भएमा (स्पष्ट गल्तीको अवस्था बाहेक), विवादको हदसम्म तालिकाका विवरणहरू लागू हुनेछन्।

१८.३. हाम्रो प्रमाणपत्रमा निर्भरता: हामीले सही गरेको कुनै पनि लिखित सूचना वा प्रमाणपत्रलाई हामी निम्न कुराहरूको प्रमाणको रूपमा लिनेछौं: क) यस ऋण सम्झौता अन्तर्गत शर्त उल्लंघन (default) भएको छ; र ख) यस ऋण सम्झौता अन्तर्गत तपाईंले तिर्न बाँकी रकम कति छ। यो तबसम्म सही मानिनेछ जबसम्म तपाईंले हामीले गल्ती गरेको प्रमाणित गर्नुहुन्न वा बाह्य विवाद समाधान निकाय वा सक्षम अदालतले अन्यथा निर्धारण गर्दैन।

१८.४. तपाईंको दायित्व निरन्तर रहन्छ: तपाईं, कुल ऋण रकम वा अन्य कुनै कुरामा जे भए पनि (जस्तै: तपाईंको मृत्यु भए वा तपाईं दिवालिया भए पनि) यस ऋण सम्झौता अन्तर्गत तपाईंको दायित्वहरू जारी रहनेछन्।

१८.५. ऋण समाप्त गर्ने (Discharge) प्रक्रिया: क) यदि तपाईंले ऋण सम्झौता औपचारिक रूपमा समाप्त गर्न (डिस्चार्ज गर्न) अनुरोध गर्नुभयो र ऋण पूर्ण रूपमा चुक्ता भएकोमा हामी सन्तुष्ट भएनौं भने, हामी तपाईंको अनुरोध प्राप्त भएको एक (१) हप्ताभित्र तपाईंको बाँकी बक्यौताको विवरण प्रस्तुत गर्नेछौं। ऋण बाँकी रकम तपाईंले पूर्ण रूपमा चुक्ता गरेपछि मात्र समाप्त हुनेछ। ख) तपाईंले हामीलाई कुनै पनि रकम तिर्न बाँकी छैन भन्नेमा हामी विश्वस्त नभएसम्म (जस्तै: अन्तिम भुक्तानी अस्वीकृत हुन सक्ने वा फिर्ता हुन सक्ने अवस्थामा) हामीले यो ऋण सम्झौता समाप्त गर्न (डिस्चार्ज) आवश्यक छैन। यो ऋण सम्झौता समाप्त भए पनि, बाँकी रहेको वा समाप्त भएपछि बाँकी हुन आउने कुनै पनि रकम अझै पनि तिर्नुपर्छ।

१८.६. अवैध प्रावधानहरू: यदि यस ऋण सम्झौताको कुनै प्रावधान गैरकानूनी, शून्य (void) वा लागू गर्न नसकिने छ भने, त्यो प्रावधान कानुनी र लागू गर्न सकिने बनाउनका लागि आवश्यक हदसम्म परिवर्तन गरिएको वा आवश्यक परेमा हटाइएको मानिने गरी यो सम्झौता पढिनेछ।

१९. व्याख्या (सर्तहरू बुझ्ने)

१९.१. परिभाषाहरू: तपाईंको ऋण सम्झौतामा: * "account" (खाता) को अर्थ तपाईंले ऋण सम्झौताको उद्देश्यका लागि हामीसँग राख्नुभएको खाता हो। * "amount of credit provided" (उपलब्ध गराइएको ऋण रकम) को अर्थ यस सम्झौताको वित्तीय तालिकामा उल्लेख गरिएको रकम हो। * "annual percentage rate" (वार्षिक प्रतिशत दर) को अर्थ तालिकामा वार्षिक प्रतिशत दरको रूपमा वर्णन गरिएको दर हो। * "arrears" (बक्यौता) को अर्थ सबै भुक्तानीहरू समयमै गरिएको भए खातामा जति ब्यालेन्स हुनुपर्थ्यो, वास्तविक ब्यालेन्स त्योभन्दा कम हुनु हो। * "balance" (ब्यालेन्स) को अर्थ खातामा जम्मा गरिएका (credited) र खाताबाट निकालिएका (debited) सबै रकमहरू बीचको भिन्नता हो। * "business day" (कारोबार दिन) को अर्थ शनिबार, आइतबार वा राष्ट्रिय सार्वजनिक बिदा बाहेकको दिन हो। * "credit fees and charges" (ऋण शुल्क र चार्जहरू) को अर्थ तपाईंको ऋण सम्झौताको तालिकामा तोकिएका शुल्कहरू हुन्। * "credit provider" (ऋण प्रदायक) को अर्थ Support Finance Pty Ltd हो। * "daily balance" (दैनिक ब्यालेन्स) को अर्थ दिनको अन्त्यमा रहेको ब्यालेन्स हो। * "disclosure date" (खुलासा मिति) को अर्थ तालिकामा उल्लेख गरिएको मिति हो। * "EDR" (बाह्य विवाद समाधान) को अर्थ हाम्रो स्वीकृत बाह्य विवाद समाधान योजना प्रदायकले प्रयोग गर्ने प्रक्रियाहरू हुन्। * "electronic address" (विद्युतीय ठेगाना) को अर्थ तपाईंले हामीलाई सम्पर्क गर्न अनुमति दिनुभएको इमेल, फ्याक्स वा मोबाइल नम्बर हो। * "General Conditions" (सामान्य शर्तहरू) को अर्थ तपाईंको ऋण सम्झौताका यी सम्पूर्ण सामान्य शर्तहरू हुन्। * "government transaction charges" (सरकारी कारोबार शुल्क) को अर्थ ऋण सम्बन्धी प्राप्ति वा निकासी (withdrawals) मा लाग्ने सरकारी शुल्क वा महसुलहरू (जस्तै स्ट्याम्प शुल्क), तपाईं तिर्न जिम्मेवार भए पनि वा नभए पनि। * "IDR" (आन्तरिक विवाद समाधान) को अर्थ हाम्रो आन्तरिक विवाद समाधान प्रक्रियाहरू हो। (EDR मा जानुअघि तपाईंले यो प्रक्रिया प्रयोग गर्नुपर्छ)। * "law" (कानुन) को अर्थ सामान्य कानुन, इक्विटीका सिद्धान्तहरू र कुनै पनि सरकारी निकाय वा प्राधिकरणले बनाएका सबै कानुनहरू समावेश छन्। * "legislation" (विधायन) को अर्थ कुनै पनि सरकारी निकाय वा प्राधिकरणले बनाएका सबै ऐन, नियम वा विनियमहरू समावेश छन्। * "loan" (ऋण) को अर्थ यस ऋण सम्झौता अन्तर्गत उपलब्ध गराइएको वा गरिने ऋण रकम हो। * "loan contract" (ऋण सम्झौता) को अर्थ तपाईं र हामी दुवैले सही गरेपछि यो सम्पूर्ण क्रेडिट सम्झौता हो। * "National Credit Code" (राष्ट्रिय ऋण संहिता) को अर्थ National Consumer Credit Protection Act 2009 को अनुसूची १ हो। * "party" (पक्ष) को अर्थ तपाईं वा हामी मध्ये कुनै एक हो। * "Schedule" (तालिका) को अर्थ तपाईंको ऋण सम्झौताको साथमा संलग्न तालिका हो। * "Settlement date" (निपटान मिति) को अर्थ ऋण (वा यसको कुनै अंश) पहिलो पटक तपाईंको खातामा डेबिट गरिएको मिति हो। * "State" (राज्य) को अर्थ अष्ट्रेलियाको कुनै पनि राज्य वा क्षेत्र हो। * "total amount owing" (कुल तिर्नुपर्ने रकम) को अर्थ यस ऋण सम्झौता वा तपाईंले हामीलाई दायित्व तिर्नुपर्ने वा हामीले तपाईं विरुद्ध अधिकार राख्ने अन्य कुनै पनि कागजात अन्तर्गत तपाईंले हामीलाई तिर्न बाँकी सबै रकमहरू हो (राष्ट्रिय ऋण संहिताले समावेश गर्न निषेध गरेका रकमहरू बाहेक)। * "us", "our", र "we" (हामी, हाम्रो) को अर्थ Support Finance Pty Ltd हो। * "you" (तपाईं) को अर्थ तालिकामा नाम उल्लेख गरिएका प्रत्येक ऋण लिने व्यक्ति हो।

१९.२. सम्झौता पढ्ने सामान्य नियमहरू: क) शीर्षकहरू सजिलोका लागि मात्र हुन् र यस सम्झौताको व्याख्यालाई असर गर्दैनन्। ख) एक वचनले बहुवचनलाई पनि बुझाउँछ र त्यसको उल्टो पनि। ग) कुनै व्यक्तिको सन्दर्भमा प्राकृतिक व्यक्ति र निगम (कम्पनी) दुवै समावेश हुन्छ। घ) कुनै कागजात वा सम्झौताको सन्दर्भमा त्यसका सबै परिवर्तन वा प्रतिस्थापनहरू समावेश हुन्छन्। ङ) यहाँ प्रयोग गरिएका शब्द वा वाक्यांशहरूको तालिका र राष्ट्रिय ऋण संहितामा भएको अर्थ नै हुनेछ। च) कुनै पनि व्यक्तिको सन्दर्भमा (तपाईं वा हामी सहित) त्यस व्यक्तिका उत्तराधिकारी वा कानुनी प्रतिनिधिहरू समावेश हुन्छन्।

१९.३. "includes" (समावेश गर्दछ) भन्ने शब्द उदाहरणका लागि दिइएको हो र यसले यसमा लागू हुने शब्दलाई सीमित गर्दैन।

यस पृष्ठको बाँकी भाग जानाजानी खाली राखिएको छ।

Recent Articles

Court Marriage Certificate

Dec 25, 2025

Notary: Letter to Immigration

Dec 25, 2025

Translation: Human Trafficking

Dec 12, 2025

Translation: Contract

Dec 11, 2025